Financial Planning

back

Yield to maturity (YTM) is considered a long-term bond yield but is expressed as an annual rate. It is the internal rate of return (IRR) of an investment in a bond if the investor holds the bond until maturity, with all payments made as scheduled and reinvested at the same rate.

Yield to maturity is also referred to as book yield or redemption yield. YTM accounts for the present value of a bond's future coupon payments and factors in the time value of money,

KEY TAKEAWAYS

Important: Bonds are priced at a discount, at par, or a premium. At par, the bond's interest rate equals its coupon rate. Above par, the bond is called a premium bond with a coupon rate higher than the realized interest rate. A bond priced below par, called a discount bond, has a coupon rate lower than the realized interest rate.

To calculate YTM on a bond priced below par, investors plug in various annual interest rates higher than the coupon rate to find a bond price close to the researched bond price. Calculations of yield to maturity assume that all coupon payments are reinvested at the same rate as the bond's current yield and account for the bond's current market price, par value, coupon interest rate, and term to maturity.

The YTM is a snapshot of the return on a bond because coupon payments cannot always be reinvested at the same interest rate. As interest rates rise, the YTM will increase; as interest rates fall, the YTM will decrease. Investors can approximate YTM using a bond yield table, financial calculator, or online YTM calculator.

Unlike stock investments, bond issuers promise to pay the holder the full face value once it matures. Bonds come with two metrics: YTM and coupon rate. YTM is the total return expected on a bond if it's held until maturity.

The coupon rate is the total amount the bond pays in income to the bondholder for as long as they hold it. The coupon rate is the interest paid annually on the bond's face value. A bond's YTM fluctuates over time. The coupon rate remains fixed.

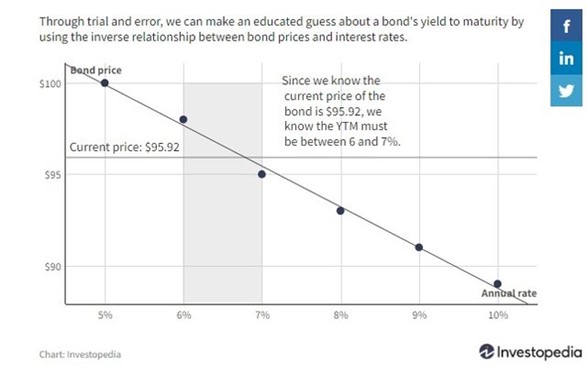

An investor holds a bond whose par value is $100. The bond is priced at a discount of $95.92, matures in 30 months, and pays a semi-annual coupon of 5%. Therefore, the current yield of the bond is (5% coupon x $100 par value) / $95.92 market price = 5.21%.

To calculate YTM, the cash flows must be determined first. Every six months (semi-annually), the bondholder receives a coupon payment of (5% x $100)/2 = $2.50. In total, they receive five payments of $2.50, in addition to the face value of the bond due at maturity, which is $100. Next, we incorporate this data into the formula:

In this example, the par value of the bond is $100, but it is priced below the par value at $95.92, meaning the bond is priced at a discount. The annual interest rate must be greater than the coupon rate of 5%. Investors calculate and test several bond prices by plugging various annual interest rates that are higher than 5% into the formula above:

Taking the interest rate up by one and two percentage points to 6% and 7% yields bond prices of $98 and $95, respectively. Because the bond price in the example is $95.92, the list indicates that the interest rate is between 6% and 7%.

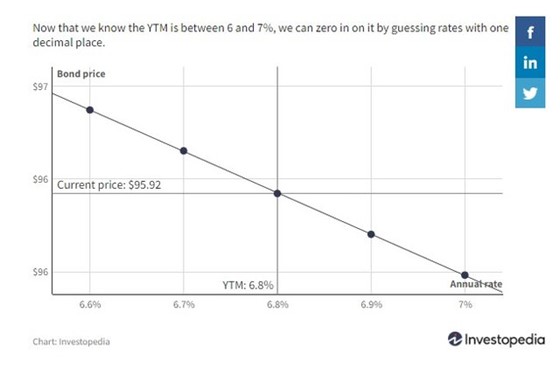

Having determined the range of rates, investors take a closer look and make another table showing the prices where YTM calculations produce a series of interest rates increasing in increments of 0.1% instead of 1.0%. Using interest rates with smaller increments, calculated bond prices are as follows:

The present value of this bond is equal to $95.92 when the YTM is at 6.8%. Fortunately, 6.8% corresponds precisely to the bond price, so no further calculations are required. If the investor found that using a YTM of 6.8% in their calculations did not yield the exact bond price, they would continue trials and test interest rates increasing in 0.01% increments.

Yield to maturity has variations that account for bonds with embedded options:

YTM calculations usually do not account for taxes that an investor pays on the bond. In this case, YTM is known as the gross redemption yield. YTM calculations also do not account for purchasing or selling costs. YTM makes assumptions about the future, and an investor may not be able to reinvest all coupons, the bond may not be held to maturity, and the bond issuer may default.

The main difference between the YTM of a bond and its coupon rate is that the coupon rate is fixed and the YTM fluctuates. The coupon rate is contractually fixed, whereas the YTM changes based on the price paid for the bond and the interest rates available in the marketplace.

A bond's yield to maturity is the internal rate of return required for the present value of all future cash flows, including face value and coupon payments, to equal the current bond price. YTM assumes that all coupon payments are reinvested at a yield equal to the YTM and that the bond is held to maturity. Bond investments include municipal, treasury, corporate, and foreign.

Cover Photo: Jessica Olah, Investopedia

Yield to Maturity (YTM): What It Is and How It Works

What Is Yield to Maturity (YTM)?

Yield to maturity (YTM) is considered a long-term bond yield but is expressed as an annual rate. It is the internal rate of return (IRR) of an investment in a bond if the investor holds the bond until maturity, with all payments made as scheduled and reinvested at the same rate.

Yield to maturity is also referred to as book yield or redemption yield. YTM accounts for the present value of a bond's future coupon payments and factors in the time value of money,

KEY TAKEAWAYS

- Yield to maturity is the total rate of return earned when a bond makes all interest payments and repays the original principal.

- YTM is essentially a bond's internal rate of return if held to maturity.

- Calculating the yield to maturity assumes all coupon or interest payments can be reinvested at the same rate of return as the bond.

YTM Formulas

Important: Bonds are priced at a discount, at par, or a premium. At par, the bond's interest rate equals its coupon rate. Above par, the bond is called a premium bond with a coupon rate higher than the realized interest rate. A bond priced below par, called a discount bond, has a coupon rate lower than the realized interest rate.

Calculating YTM

To calculate YTM on a bond priced below par, investors plug in various annual interest rates higher than the coupon rate to find a bond price close to the researched bond price. Calculations of yield to maturity assume that all coupon payments are reinvested at the same rate as the bond's current yield and account for the bond's current market price, par value, coupon interest rate, and term to maturity.

The YTM is a snapshot of the return on a bond because coupon payments cannot always be reinvested at the same interest rate. As interest rates rise, the YTM will increase; as interest rates fall, the YTM will decrease. Investors can approximate YTM using a bond yield table, financial calculator, or online YTM calculator.

YTM vs. Coupon Rate

Unlike stock investments, bond issuers promise to pay the holder the full face value once it matures. Bonds come with two metrics: YTM and coupon rate. YTM is the total return expected on a bond if it's held until maturity.

The coupon rate is the total amount the bond pays in income to the bondholder for as long as they hold it. The coupon rate is the interest paid annually on the bond's face value. A bond's YTM fluctuates over time. The coupon rate remains fixed.

Trial and Error Example

An investor holds a bond whose par value is $100. The bond is priced at a discount of $95.92, matures in 30 months, and pays a semi-annual coupon of 5%. Therefore, the current yield of the bond is (5% coupon x $100 par value) / $95.92 market price = 5.21%.

To calculate YTM, the cash flows must be determined first. Every six months (semi-annually), the bondholder receives a coupon payment of (5% x $100)/2 = $2.50. In total, they receive five payments of $2.50, in addition to the face value of the bond due at maturity, which is $100. Next, we incorporate this data into the formula:

In this example, the par value of the bond is $100, but it is priced below the par value at $95.92, meaning the bond is priced at a discount. The annual interest rate must be greater than the coupon rate of 5%. Investors calculate and test several bond prices by plugging various annual interest rates that are higher than 5% into the formula above:

Taking the interest rate up by one and two percentage points to 6% and 7% yields bond prices of $98 and $95, respectively. Because the bond price in the example is $95.92, the list indicates that the interest rate is between 6% and 7%.

Having determined the range of rates, investors take a closer look and make another table showing the prices where YTM calculations produce a series of interest rates increasing in increments of 0.1% instead of 1.0%. Using interest rates with smaller increments, calculated bond prices are as follows:

The present value of this bond is equal to $95.92 when the YTM is at 6.8%. Fortunately, 6.8% corresponds precisely to the bond price, so no further calculations are required. If the investor found that using a YTM of 6.8% in their calculations did not yield the exact bond price, they would continue trials and test interest rates increasing in 0.01% increments.

Variations of YTM

Yield to maturity has variations that account for bonds with embedded options:

- Yield To Call (YTC): Assumes the bond will be called and repurchased by the issuer before it reaches maturity and thus has a shorter cash flow period. YTC is calculated, assuming the bond will be called as soon as possible and financially feasible.

- Yield To Put (YTP): Similar to YTC, however, the holder of a put bond can sell the bond back to the issuer at a fixed price based on the terms of the bond. YTP is calculated based on the assumption that the bond will be put back to the issuer as soon as possible and financially feasible.

- Yield To Worst (YTW): A calculation used when a bond has multiple options. If an investor evaluates a bond with both call and put provisions, they would calculate the YTW based on the option terms that give the lowest yield.

What Are Limitations of YTM?

YTM calculations usually do not account for taxes that an investor pays on the bond. In this case, YTM is known as the gross redemption yield. YTM calculations also do not account for purchasing or selling costs. YTM makes assumptions about the future, and an investor may not be able to reinvest all coupons, the bond may not be held to maturity, and the bond issuer may default.

What Is the Difference Between a Bond’s YTM and Its Coupon Rate?

The main difference between the YTM of a bond and its coupon rate is that the coupon rate is fixed and the YTM fluctuates. The coupon rate is contractually fixed, whereas the YTM changes based on the price paid for the bond and the interest rates available in the marketplace.

What Does a Higher YTM Indicate?

Whether or not a higher YTM is positive depends on specific circumstances. A higher YTM might indicate a bargain opportunity is available since the bond in question is available for less than its par value. However, investors must determine whether or not this discount is justified by fundamentals such as the creditworthiness of the company issuing the bond, or the interest rates presented by alternative investments.The Bottom Line

A bond's yield to maturity is the internal rate of return required for the present value of all future cash flows, including face value and coupon payments, to equal the current bond price. YTM assumes that all coupon payments are reinvested at a yield equal to the YTM and that the bond is held to maturity. Bond investments include municipal, treasury, corporate, and foreign.