Financial Planning

back

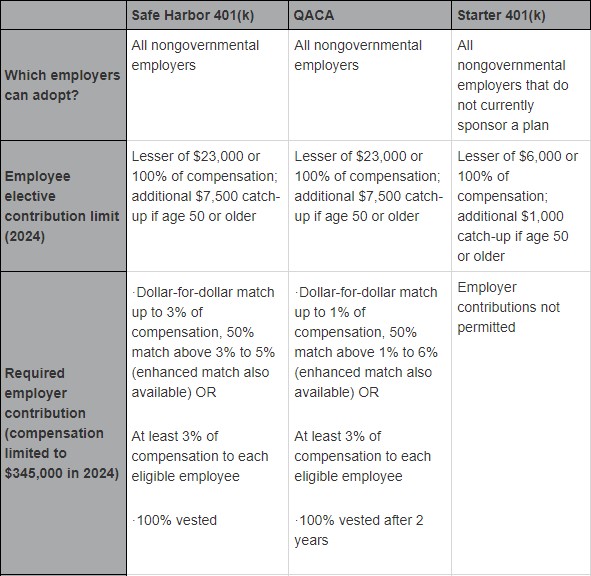

Small business owners looking to adopt 401(k) plans are sometimes discouraged by the typically high costs and complicated testing requirements associated with plan administration (see sidebar). Fortunately, over the past few decades, legislators have introduced a number of simplified alternatives to the traditional 401(k) to help encourage more business owners to adopt these potentially valuable retirement benefit programs. Among them are the safe harbor plan, the qualified automatic contribution arrangement (QACA), and most recently, the starter 401(k) plan.

In a traditional 401(k) plan, you're not required to make employer contributions. Safe harbor plans allow you to avoid testing by making fully vested contributions on behalf of employees.

You have several options. First, you can make a nonelective contribution of 3% (or more) of pay for each eligible employee, even those who aren't actively contributing. Alternatively, you can match employee contributions dollar for dollar up to 3% of pay and match contributions from 3% to 5% of pay at a 50% rate (the "basic match"). You also have the option of making an "enhanced" matching contribution that is at least as generous as the basic match.

Election change

With a safe harbor plan, you can decide as late as 30 days prior to the end of a plan year whether you'll use the 3% nonelective safe harbor for that year, which could be useful if you want to see how your testing is progressing before you commit to a safe harbor contribution for the year. Alternatively, your plan may be amended as late as the end of the year following the plan year, but only if the nonelective safe harbor contribution is 4%.

Employee contributions

As with traditional 401(k) plans, employees in safe harbor 401(k) plans can contribute up to $23,000 in 2024, plus an additional $7,500 for those age 50 and older ($22,500 and $7,500, respectively, for 2023).

A QACA is a safe harbor 401(k) plan with an automatic enrollment feature. While most of the rules applicable to safe harbor plans also apply to QACAs, there are some notable exceptions.

Under a QACA, an employee who fails to make an affirmative deferral election is automatically enrolled in the plan. An employee's automatic contribution must be at least 3% for the first two calendar years of participation and then increase 1% each year until it reaches 6%. You can require an automatic contribution of as much as 15%.

Employees can change their contribution rate or stop contributing at any time and get a refund of their automatic contributions if they opt out within 90 days.

Your required employer contribution is either 3% of pay to each eligible employee or a dollar-for-dollar matching contribution up to 1% of pay and 50% on additional contributions of up to 6% of pay. You may also impose a two-year vesting schedule (compared to immediate vesting in a safe harbor plan). And if you select certain default investments for employee contributions, you'll generally be relieved of fiduciary responsibility for any losses your employees incur from those investments.

Beginning in 2024, employers with no other retirement plan (with limited exceptions) can adopt what's known as a starter 401(k) plan. Designed to be low cost and easy to administer, starter 401(k) plans allow only employee contributions. Employees must be auto-enrolled at a minimum contribution rate of 3% (not to exceed 15%) and may contribute up to $6,000 in 2024 ($7,000 for employees age 50 or older).

Sidebar

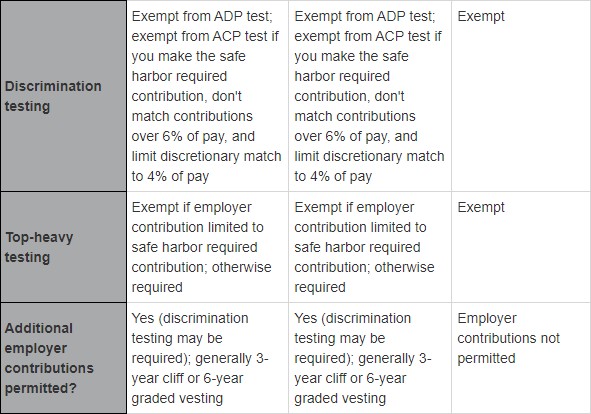

Traditional 401(k) plans are required to undergo testing each year to make sure the plans do not favor highly compensated employees (HCEs) and key employees over the rank-and-file non-HCEs. There are three primary tests: the actual deferral percentage (ADP) test, the actual contribution percentage (ACP) test, and the top-heavy test. The ACP and ADP tests are designed to compare plan utilization by HCEs and non-HCEs to ensure that usage is widespread and benefits all plan participants. The top-heavy test gauges the percentage of total plan assets that can be attributed to key employees.

The SECURE Act 2.0 signed in late 2022 ushered in two new tax credits for small employers adopting a retirement savings plan, one for plan startup costs and one for employer contributions. Now might be an ideal time to consider adopting a 401(k) plan for yourself and your employees to take advantage of these credits.

This content has been reviewed by FINRA.

Prepared by Broadridge Advisor Solutions. © 2024 Broadridge Financial Services, Inc.

401(k) Plans for Small Businesses

Safe Harbor Plan

In a traditional 401(k) plan, you're not required to make employer contributions. Safe harbor plans allow you to avoid testing by making fully vested contributions on behalf of employees.

You have several options. First, you can make a nonelective contribution of 3% (or more) of pay for each eligible employee, even those who aren't actively contributing. Alternatively, you can match employee contributions dollar for dollar up to 3% of pay and match contributions from 3% to 5% of pay at a 50% rate (the "basic match"). You also have the option of making an "enhanced" matching contribution that is at least as generous as the basic match.

Election change

With a safe harbor plan, you can decide as late as 30 days prior to the end of a plan year whether you'll use the 3% nonelective safe harbor for that year, which could be useful if you want to see how your testing is progressing before you commit to a safe harbor contribution for the year. Alternatively, your plan may be amended as late as the end of the year following the plan year, but only if the nonelective safe harbor contribution is 4%.

Employee contributions

As with traditional 401(k) plans, employees in safe harbor 401(k) plans can contribute up to $23,000 in 2024, plus an additional $7,500 for those age 50 and older ($22,500 and $7,500, respectively, for 2023).

QACAs

A QACA is a safe harbor 401(k) plan with an automatic enrollment feature. While most of the rules applicable to safe harbor plans also apply to QACAs, there are some notable exceptions.

Under a QACA, an employee who fails to make an affirmative deferral election is automatically enrolled in the plan. An employee's automatic contribution must be at least 3% for the first two calendar years of participation and then increase 1% each year until it reaches 6%. You can require an automatic contribution of as much as 15%.

Employees can change their contribution rate or stop contributing at any time and get a refund of their automatic contributions if they opt out within 90 days.

Your required employer contribution is either 3% of pay to each eligible employee or a dollar-for-dollar matching contribution up to 1% of pay and 50% on additional contributions of up to 6% of pay. You may also impose a two-year vesting schedule (compared to immediate vesting in a safe harbor plan). And if you select certain default investments for employee contributions, you'll generally be relieved of fiduciary responsibility for any losses your employees incur from those investments.

Starter 401(k) Plans

Beginning in 2024, employers with no other retirement plan (with limited exceptions) can adopt what's known as a starter 401(k) plan. Designed to be low cost and easy to administer, starter 401(k) plans allow only employee contributions. Employees must be auto-enrolled at a minimum contribution rate of 3% (not to exceed 15%) and may contribute up to $6,000 in 2024 ($7,000 for employees age 50 or older).

Sidebar

Traditional 401(k) plans are required to undergo testing each year to make sure the plans do not favor highly compensated employees (HCEs) and key employees over the rank-and-file non-HCEs. There are three primary tests: the actual deferral percentage (ADP) test, the actual contribution percentage (ACP) test, and the top-heavy test. The ACP and ADP tests are designed to compare plan utilization by HCEs and non-HCEs to ensure that usage is widespread and benefits all plan participants. The top-heavy test gauges the percentage of total plan assets that can be attributed to key employees.

The SECURE Act 2.0 signed in late 2022 ushered in two new tax credits for small employers adopting a retirement savings plan, one for plan startup costs and one for employer contributions. Now might be an ideal time to consider adopting a 401(k) plan for yourself and your employees to take advantage of these credits.

This content has been reviewed by FINRA.

Prepared by Broadridge Advisor Solutions. © 2024 Broadridge Financial Services, Inc.