Financial Planning

back

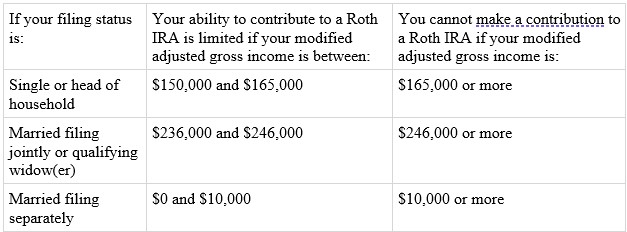

Maybe. It depends on your particular circumstances. You must have earned income during the year (typically, wages or self-employment income). Beyond that, your eligibility for a Roth IRA will hinge on two primary considerations: your adjusted gross income for the year and your income tax filing status. In a given tax year, it's possible you may qualify to contribute the maximum amount allowed by law, a lesser amount, or nothing at all. The maximum contribution is $7,000 in 2025 (unchanged from 2024). In addition, if you're age 50 or older, you can make an extra "catch-up" contribution of $1,000 in 2025 (unchanged from 2024).

Your allowable Roth IRA contribution for a given year may be reduced by contributions made to other IRAs during the same tax year. For example, even if you qualify to contribute the full $7,000 to a Roth IRA in 2025, you will be able to put in only $1,000 if you've already contributed $6,000 to your traditional IRA for that same year (assuming you're not age 50 or older in 2025).

This content has been reviewed by FINRA.

Can I contribute to a Roth IRA?

Your allowable Roth IRA contribution for a given year may be reduced by contributions made to other IRAs during the same tax year. For example, even if you qualify to contribute the full $7,000 to a Roth IRA in 2025, you will be able to put in only $1,000 if you've already contributed $6,000 to your traditional IRA for that same year (assuming you're not age 50 or older in 2025).