Financial Planning

back

Here's the good news about health care in retirement: 94% of Medicare beneficiaries age 65 and up are satisfied with their quality of care.1 The not-so-good news? The government health insurance program doesn't cap costs, potentially exposing many retirees to higher-than-expected out-of-pocket expenses.

Indeed, a couple with average Medicare premiums and out-of-pocket expenses may need between $212,000 and $318,000 in savings to cover their health expenses throughout retirement, according to an analysis by the Employee Benefit Research Institute.2

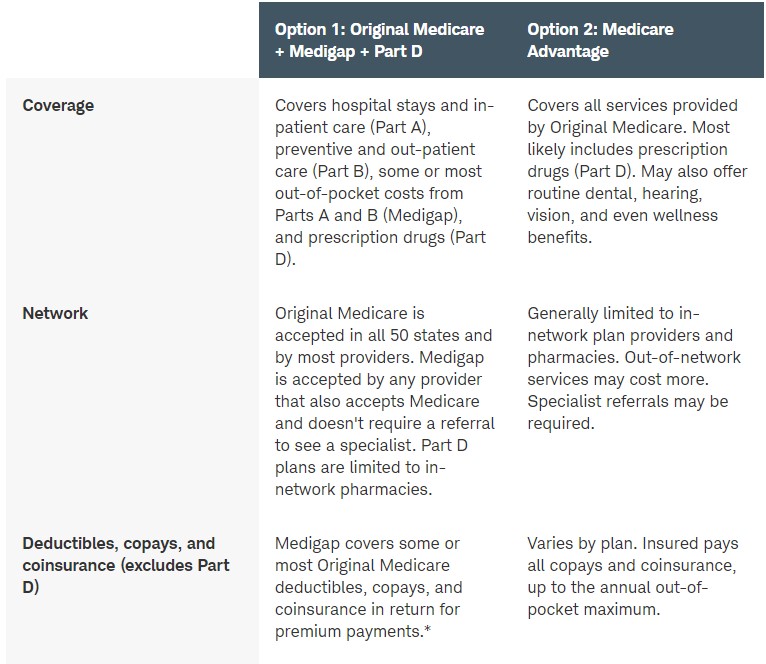

Then again, Medicare was never intended to cover all health care services. Introduced in 1965, the program offered basic insurance to retirees who otherwise lacked coverage. Over the years, Congress has greatly expanded the pool of eligible participants, but Original Medicare still covers only certain services, including hospital stays (under what's known as Part A) and outpatient medical care (under Part B). Services outside its scope—including routine dental and vision care, prescription drugs taken at home, and long-term care—must be paid out of pocket or via a separate private insurance policy.

To complicate matters, Medicare isn't retirees' only option. Private insurance policies, known as Medicare Advantage plans (a.k.a. Part C), cover the same services as Original Medicare, generally include prescription drug coverage, and cap out-of-pocket expenses. (Some plans also offer additional coverage, such as dental and vision.) But these plans have drawbacks, including limited provider networks and a higher incidence of coverage denial.

"Choosing the right Medicare coverage is critical because it affects the doctors you'll see, the hospitals you'll go to, and the costs you'll pay out of pocket—often over the remainder of your lifetime," says Chris Kawashima, CFP®, a senior research analyst at the Schwab Center for Financial Research. "To maximize coverage and minimize out-of-pocket costs—which can be substantial—there are really just two main options."

It works in any state with any provider who accepts Medicare.

You can see specialists directly, without prior approval from a primary care provider (PCP).

Coverage is transparent, and you'll pay a relatively predictable amount, no matter what level of care you require.

If you're healthy, don't have many prescriptions, and/or don't need a lot of medical care in early retirement, you'll still pay Medigap and Part D premiums even if you don't access those benefits.

If you want routine dental, hearing, and/or vision coverage, you'll need to purchase it separately through a private insurer.

Part A typically has no premiums, so long as you or your spouse paid Medicare taxes for at least 10 years while working. There's a deductible for each hospital stay ($1,600 in 2023), along with a daily copay for stays of more than 60 days—starting at $400 per day and increasing to 100% of the bill for stays of 150 days or longer.

Part B requires income-based premium payments, starting at $164.90 per month in 2023 but going as high as $560.50 for wealthy individuals. There's an annual deductible of $226 in 2023, after which you'll generally be responsible for 20% of outpatient bills—though certain services, including some preventive care, won't cost you anything.

To help manage costs, you can purchase a private Medicare Supplement Plan (a.k.a. Medigap), which will cover some or most out-of-pocket expenses incurred from Original Medicare, depending on which of several standardized policies you choose. Premiums vary widely based on level of coverage, as well as age, health, location, sex, and whether your acceptance is guaranteed or subject to review.

For example, a person in Chicago who chooses a Medigap Plan G policy—which provides the most comprehensive coverage for newly eligible Medicare recipients—can expect to pay between $109 and $748 per month, whereas a person in Miami can expect to pay between $228 and $1,820 for the same plan.3

If you want a prescription drug plan, you'll have to purchase a private policy (Part D) at an average monthly cost of $43—though, as with Original Medicare, retirees with higher incomes should expect to pay more.

The higher your income, the more Part B and Part D will cost you.

2021 inc, single filer 2021 inc, married file jointly Part B premium Part D premium

$97,000 or less $194,000 or less $164.90 Plan prem. (varies by provider)

$97,001 to $123,000 $194,001 to $246,000 $230.80 Plan premium + $12.20

$123,001 to $153,000 $246,001 to $306,000 $329.70 Plan premium + $31.50

$153,001 to $183,000 $306,001 to $366,000 $428.60 Plan premium + $50.70

$183,001 to $499,999 $366,001 to $749,999 $527.50 Plan premium + $70.00

$500,000 or more $750,000 or more $560.50 Plan premium + $76.40

Source:

Medicare.gov.The 2023 premiums are determined by the recipient's 2021 modified adjusted gross income. Premiums are per individual

Timing: If you begin Social Security benefits before age 65, you'll automatically be enrolled in Medicare Parts A and B when you turn 65. Otherwise, you must enroll during your initial enrollment period (IEP)—a seven-month period starting three months before you turn 65 and ending three months after your birthday—during which you should also enroll in Part D.

If you have health insurance through your or your spouse's employer, you may be able to delay Medicare enrollment. Once you lose your workplace coverage, you'll have eight months to sign up for Medicare (but only two months for Part D) during a special enrollment period (SEP). However, the rules around such a move can be complicated, so it's best to speak with your HR department about whether you should still sign up during your IEP.

If you don't sign up during your IEP or SEP, you'll usually have to wait for the general enrollment period, which runs from January 1 to March 31 each year. Even so, waiting beyond your initial eligibility can be costly:

For every full year you delay enrolling in Part B, you'll pay 10% more for the same coverage—for life.4

Part D also has a late-enrollment penalty, which is calculated by multiplying 1% of the average national base premium—a figure released annually by Medicare ($32.74 in 2023)—by the number of months without creditable coverage. You'll pay this fee on top of your monthly premium for as long as you have prescription drug coverage, whether on its own or through Medicare Advantage.

For Medigap, it's best to enroll within six months of signing up for Part B, during which time you have guaranteed acceptance to any Medigap policy you choose. After that, you can enroll anytime without penalty, but you're likely to face higher premiums—and could be denied coverage.

The Takeaway

"Opting into Original Medicare and purchasing Medigap and Part D generally is a good strategy if you have a preexisting condition, believe your health may deteriorate, or want greater certainty around your out-of-pocket costs and a wider choice of doctors and hospitals," Chris says.

Option 2: Medicare Advantage

The Pros

You'll generally pay less in monthly premiums than you would with Option 1.

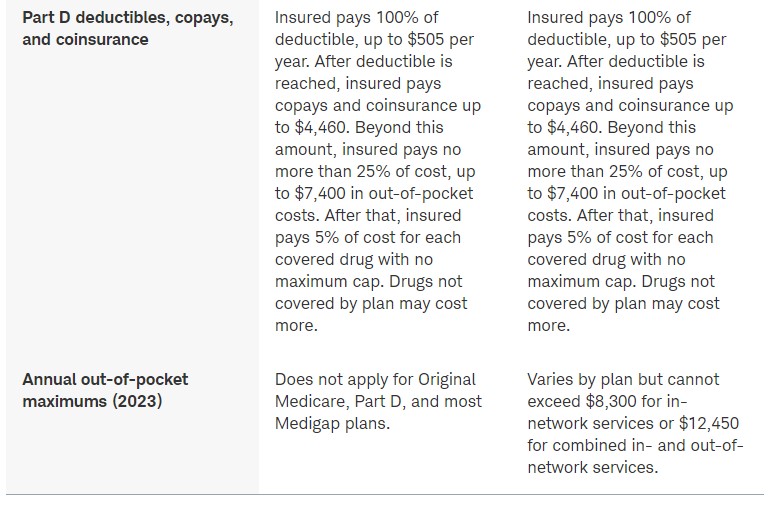

Medicare Advantage plans cap annual out-of-pocket spending—though it can be as high as $8,300 a year for in-network services and $12,450 for combined in- and out-of-network services. (National averages are $4,972 for in-network and $9,245 for out-of-network services.5) Prescription drug coverage is subject to different rules.

Coverage may include prescription drugs and other services not covered by Medicare, such as dental and vision care.

The Cons

Medicare Advantage plans generally limit heath care access to a network of providers in your area. This can be an issue if you want to keep your PCP or spend substantial time away from your primary residence.

You may need a referral from your PCP before you can see a specialist.

Medicare Advantage plans may have a higher incidence of coverage denial.

If you decide later to switch to Option 1, you may pay a higher premium for a Medigap plan, assuming you qualify.

Coverage and costs: Medicare Advantage plans bundle parts A, B, and often D, plus other services not covered by Original Medicare, such as routine dental and vision. On average, the typical beneficiary in 2023 has a choice of 43 plans, according to research by the Kaiser Family Foundation. Premiums average about $18 per month on top of your Part B premium, but in many plans, the premium can be as low as $0.

Unlike with Option 1—whereby you pay higher premiums for benefits you may not need right away—you'll incur the bulk of Medicare Advantage costs when you use your coverage, via coinsurance and copays.

Timing: If you opt for a Medicare Advantage plan from the start, you'll sign up for it along with Medicare Part A and Part B during your IEP, or during a two-month SEP. If you decide to opt in later, you can do so during the open enrollment period that runs from October 15 through December 7 each year. You can also switch plans, or even switch to Original Medicare, during the annual open enrollment window.

"For someone who is generally healthy now and expects to remain so in the future, Medicare Advantage may be a good way to go," Chris says. "But betting on your continued good health may or may not pay off."

When deciding among your health care options, consider your and your family's health history, the network of health care professionals you'd like to use, your financial situation, and your tolerance for risk regarding potential out-of-pocket costs.

You should also look beyond the here and now. "Think of your needs on a continuum—from early to late retirement," Chris says. For example, you may not need prescription coverage at the start of retirement, but if you wait to enroll until you need it, you could face a much steeper premium.

Even after you make your decision, it's wise to review your coverage each year. "Costs can fluctuate, doctors can go in and out of network, and prescription drug coverage can change," Chris says. Be sure to review your Evidence of Coverage and Annual Notice of Change documents from your Medicare Advantage and/or Part D plans each year, which will tell you your current coverage and what will change in the coming year.

Disclosure

*The high-deductible options for plans F, G, and J have a deductible of $2,700. Medigap Plans K and L have an out-of-pocket maximum of $6,940 and $3,470, respectively.

State Health Insurance Assistance Programs can provide unbiased information about Medicare and help walk you through your options. A health insurance broker can help you choose the best Medicare Advantage and/or Part D coverage, as well as assist with dental and vision coverage.

"All of these decisions will depend on your current and potential medical needs, the doctors you prefer, and your prescription drug regimen, so be sure to have that information at hand," Chris says.

1"Medicare-Covered Older Adults Are Satisfied With Their Coverage, Have Similar Access to Care as Privately Insured Adults Ages 50 to 64, And Fewer Report Cost-Related Problems," kff.org, 05/17/2021, www.kff.org/report-section/medicare-covered-older-adults-are-satisfied-with-their-coverage-have-similar-access-to-care-as-privately-insured-adults-ages-50-to-64-issue-brief/.

2Projected Savings Medicare Beneficiaries Need for Health Expenses Remained High in 2022, ebri.org, 02/09/2023, www.ebri.org/content/projected-savings-medicare-beneficiaries-need-for-health-expenses-remained-high-in-2022.

3"Find a Medigap Policy That Works for You," medicare.gov, www.medicare.gov/medigap-supplemental-insurance-plans/#/m?lang=en&year=2023.

4Those who owe Part A premiums and delay enrollment will pay an extra 10% each month for twice the number of years they delay.

5"Medicare Advantage in 2022: Premiums, Out-of-Pocket Limits, Cost Sharing, Supplemental Benefits, Prior Authorization, and Star Ratings," kff.org, 08/25/2022, www.kff.org/medicare/issue-brief/medicare-advantage-in-2022-premiums-out-of-pocket-limits-cost-sharing-supplemental-benefits-prior-authorization-and-star-ratings/.

Original Article: https://www.schwab.com/learn/story/demystifying-medicare-retirement

Demystifying Medicare for Retirement

Demystifying Medicare for Retirement

Compare your Medicare options and help reduce out-of-pocket costs.Here's the good news about health care in retirement: 94% of Medicare beneficiaries age 65 and up are satisfied with their quality of care.1 The not-so-good news? The government health insurance program doesn't cap costs, potentially exposing many retirees to higher-than-expected out-of-pocket expenses.

Indeed, a couple with average Medicare premiums and out-of-pocket expenses may need between $212,000 and $318,000 in savings to cover their health expenses throughout retirement, according to an analysis by the Employee Benefit Research Institute.2

Then again, Medicare was never intended to cover all health care services. Introduced in 1965, the program offered basic insurance to retirees who otherwise lacked coverage. Over the years, Congress has greatly expanded the pool of eligible participants, but Original Medicare still covers only certain services, including hospital stays (under what's known as Part A) and outpatient medical care (under Part B). Services outside its scope—including routine dental and vision care, prescription drugs taken at home, and long-term care—must be paid out of pocket or via a separate private insurance policy.

To complicate matters, Medicare isn't retirees' only option. Private insurance policies, known as Medicare Advantage plans (a.k.a. Part C), cover the same services as Original Medicare, generally include prescription drug coverage, and cap out-of-pocket expenses. (Some plans also offer additional coverage, such as dental and vision.) But these plans have drawbacks, including limited provider networks and a higher incidence of coverage denial.

"Choosing the right Medicare coverage is critical because it affects the doctors you'll see, the hospitals you'll go to, and the costs you'll pay out of pocket—often over the remainder of your lifetime," says Chris Kawashima, CFP®, a senior research analyst at the Schwab Center for Financial Research. "To maximize coverage and minimize out-of-pocket costs—which can be substantial—there are really just two main options."

Option 1: Original Medicare + Medigap + Medicare Part D

The Pros

It works in any state with any provider who accepts Medicare.You can see specialists directly, without prior approval from a primary care provider (PCP).

Coverage is transparent, and you'll pay a relatively predictable amount, no matter what level of care you require.

The Cons

If you're healthy, don't have many prescriptions, and/or don't need a lot of medical care in early retirement, you'll still pay Medigap and Part D premiums even if you don't access those benefits.If you want routine dental, hearing, and/or vision coverage, you'll need to purchase it separately through a private insurer.

Coverage and costs: Original Medicare comprises Parts A and B:

Part A typically has no premiums, so long as you or your spouse paid Medicare taxes for at least 10 years while working. There's a deductible for each hospital stay ($1,600 in 2023), along with a daily copay for stays of more than 60 days—starting at $400 per day and increasing to 100% of the bill for stays of 150 days or longer.

Part B requires income-based premium payments, starting at $164.90 per month in 2023 but going as high as $560.50 for wealthy individuals. There's an annual deductible of $226 in 2023, after which you'll generally be responsible for 20% of outpatient bills—though certain services, including some preventive care, won't cost you anything.

To help manage costs, you can purchase a private Medicare Supplement Plan (a.k.a. Medigap), which will cover some or most out-of-pocket expenses incurred from Original Medicare, depending on which of several standardized policies you choose. Premiums vary widely based on level of coverage, as well as age, health, location, sex, and whether your acceptance is guaranteed or subject to review.

For example, a person in Chicago who chooses a Medigap Plan G policy—which provides the most comprehensive coverage for newly eligible Medicare recipients—can expect to pay between $109 and $748 per month, whereas a person in Miami can expect to pay between $228 and $1,820 for the same plan.3

If you want a prescription drug plan, you'll have to purchase a private policy (Part D) at an average monthly cost of $43—though, as with Original Medicare, retirees with higher incomes should expect to pay more.

A Premium on Premiums

The higher your income, the more Part B and Part D will cost you.

2021 inc, single filer 2021 inc, married file jointly Part B premium Part D premium

$97,000 or less $194,000 or less $164.90 Plan prem. (varies by provider)

$97,001 to $123,000 $194,001 to $246,000 $230.80 Plan premium + $12.20

$123,001 to $153,000 $246,001 to $306,000 $329.70 Plan premium + $31.50

$153,001 to $183,000 $306,001 to $366,000 $428.60 Plan premium + $50.70

$183,001 to $499,999 $366,001 to $749,999 $527.50 Plan premium + $70.00

$500,000 or more $750,000 or more $560.50 Plan premium + $76.40

Source:

Medicare.gov.The 2023 premiums are determined by the recipient's 2021 modified adjusted gross income. Premiums are per individual

Timing: If you begin Social Security benefits before age 65, you'll automatically be enrolled in Medicare Parts A and B when you turn 65. Otherwise, you must enroll during your initial enrollment period (IEP)—a seven-month period starting three months before you turn 65 and ending three months after your birthday—during which you should also enroll in Part D.

If you have health insurance through your or your spouse's employer, you may be able to delay Medicare enrollment. Once you lose your workplace coverage, you'll have eight months to sign up for Medicare (but only two months for Part D) during a special enrollment period (SEP). However, the rules around such a move can be complicated, so it's best to speak with your HR department about whether you should still sign up during your IEP.

If you don't sign up during your IEP or SEP, you'll usually have to wait for the general enrollment period, which runs from January 1 to March 31 each year. Even so, waiting beyond your initial eligibility can be costly:

For every full year you delay enrolling in Part B, you'll pay 10% more for the same coverage—for life.4

Part D also has a late-enrollment penalty, which is calculated by multiplying 1% of the average national base premium—a figure released annually by Medicare ($32.74 in 2023)—by the number of months without creditable coverage. You'll pay this fee on top of your monthly premium for as long as you have prescription drug coverage, whether on its own or through Medicare Advantage.

For Medigap, it's best to enroll within six months of signing up for Part B, during which time you have guaranteed acceptance to any Medigap policy you choose. After that, you can enroll anytime without penalty, but you're likely to face higher premiums—and could be denied coverage.

The Takeaway

"Opting into Original Medicare and purchasing Medigap and Part D generally is a good strategy if you have a preexisting condition, believe your health may deteriorate, or want greater certainty around your out-of-pocket costs and a wider choice of doctors and hospitals," Chris says.Option 2: Medicare Advantage

The Pros

You'll generally pay less in monthly premiums than you would with Option 1.Medicare Advantage plans cap annual out-of-pocket spending—though it can be as high as $8,300 a year for in-network services and $12,450 for combined in- and out-of-network services. (National averages are $4,972 for in-network and $9,245 for out-of-network services.5) Prescription drug coverage is subject to different rules.

Coverage may include prescription drugs and other services not covered by Medicare, such as dental and vision care.

The Cons

Medicare Advantage plans generally limit heath care access to a network of providers in your area. This can be an issue if you want to keep your PCP or spend substantial time away from your primary residence.You may need a referral from your PCP before you can see a specialist.

Medicare Advantage plans may have a higher incidence of coverage denial.

If you decide later to switch to Option 1, you may pay a higher premium for a Medigap plan, assuming you qualify.

Coverage and costs: Medicare Advantage plans bundle parts A, B, and often D, plus other services not covered by Original Medicare, such as routine dental and vision. On average, the typical beneficiary in 2023 has a choice of 43 plans, according to research by the Kaiser Family Foundation. Premiums average about $18 per month on top of your Part B premium, but in many plans, the premium can be as low as $0.

Unlike with Option 1—whereby you pay higher premiums for benefits you may not need right away—you'll incur the bulk of Medicare Advantage costs when you use your coverage, via coinsurance and copays.

Timing: If you opt for a Medicare Advantage plan from the start, you'll sign up for it along with Medicare Part A and Part B during your IEP, or during a two-month SEP. If you decide to opt in later, you can do so during the open enrollment period that runs from October 15 through December 7 each year. You can also switch plans, or even switch to Original Medicare, during the annual open enrollment window.

The Takeaway

"For someone who is generally healthy now and expects to remain so in the future, Medicare Advantage may be a good way to go," Chris says. "But betting on your continued good health may or may not pay off."

It's All About You

When deciding among your health care options, consider your and your family's health history, the network of health care professionals you'd like to use, your financial situation, and your tolerance for risk regarding potential out-of-pocket costs.

You should also look beyond the here and now. "Think of your needs on a continuum—from early to late retirement," Chris says. For example, you may not need prescription coverage at the start of retirement, but if you wait to enroll until you need it, you could face a much steeper premium.

Even after you make your decision, it's wise to review your coverage each year. "Costs can fluctuate, doctors can go in and out of network, and prescription drug coverage can change," Chris says. Be sure to review your Evidence of Coverage and Annual Notice of Change documents from your Medicare Advantage and/or Part D plans each year, which will tell you your current coverage and what will change in the coming year.

Medicare Options at a Glance

Disclosure

*The high-deductible options for plans F, G, and J have a deductible of $2,700. Medigap Plans K and L have an out-of-pocket maximum of $6,940 and $3,470, respectively.

Next steps

State Health Insurance Assistance Programs can provide unbiased information about Medicare and help walk you through your options. A health insurance broker can help you choose the best Medicare Advantage and/or Part D coverage, as well as assist with dental and vision coverage.

"All of these decisions will depend on your current and potential medical needs, the doctors you prefer, and your prescription drug regimen, so be sure to have that information at hand," Chris says.

1"Medicare-Covered Older Adults Are Satisfied With Their Coverage, Have Similar Access to Care as Privately Insured Adults Ages 50 to 64, And Fewer Report Cost-Related Problems," kff.org, 05/17/2021, www.kff.org/report-section/medicare-covered-older-adults-are-satisfied-with-their-coverage-have-similar-access-to-care-as-privately-insured-adults-ages-50-to-64-issue-brief/.

2Projected Savings Medicare Beneficiaries Need for Health Expenses Remained High in 2022, ebri.org, 02/09/2023, www.ebri.org/content/projected-savings-medicare-beneficiaries-need-for-health-expenses-remained-high-in-2022.

3"Find a Medigap Policy That Works for You," medicare.gov, www.medicare.gov/medigap-supplemental-insurance-plans/#/m?lang=en&year=2023.

4Those who owe Part A premiums and delay enrollment will pay an extra 10% each month for twice the number of years they delay.

5"Medicare Advantage in 2022: Premiums, Out-of-Pocket Limits, Cost Sharing, Supplemental Benefits, Prior Authorization, and Star Ratings," kff.org, 08/25/2022, www.kff.org/medicare/issue-brief/medicare-advantage-in-2022-premiums-out-of-pocket-limits-cost-sharing-supplemental-benefits-prior-authorization-and-star-ratings/.

Original Article: https://www.schwab.com/learn/story/demystifying-medicare-retirement