Financial Planning

back

Included in the Affordable Care Act (ACA) is the creation of a Health Insurance Exchange or Marketplace through which individuals and families can compare health insurance policies and purchase coverage. The ACA also provides premium tax credits and cost-sharing subsidies to help reduce the cost of premiums and out-of-pocket expenses for health coverage.

Eligible individuals and families purchasing insurance through a Marketplace may be entitled to a premium tax credit (PTC) that can reduce the cost of insurance. If you qualify, you can elect to have the credit amount paid to your insurance company to decrease monthly premiums, or you can claim the PTC on your tax return.

Eligibility for the PTC is based on the following requirements:

· You must be a U.S. citizen or have proof of legal residency and you must buy health insurance through a Marketplace

· Your household modified adjusted gross income is within a certain range based on the Federal Poverty Level (FPL)

· You are not eligible for minimum, qualifying insurance coverage through your employer or a government program such as Medicare or Medicaid

· If you are married, you and your spouse file a joint tax return

· You are not claimed as a dependent by another person

Whether you qualify for a PTC depends on your household income and family size. Income limits are based on a percentage of the FPL. Household income is your modified adjusted gross income (MAGI) plus the income of every other individual in your family who files an income tax return and for whom you claim a personal exemption deduction. MAGI is essentially your adjusted gross income plus any excluded foreign income, nontaxable Social Security benefits, and tax-exempt interest.

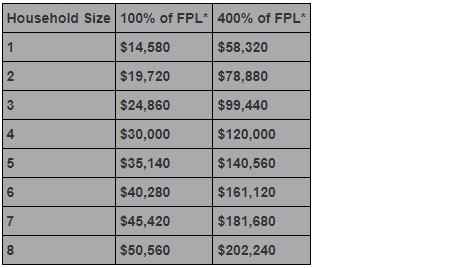

If your MAGI falls between 100% and 400% of the FPL, you may be entitled to a PTC. The following table illustrates the relationship between income as a percentage of FPL and household size. Incomes that qualify for tax credits are higher in Alaska and Hawaii.

If your income falls within the FPL parameters, the premium you're required to pay for insurance purchased through a Marketplace is reflected as a percentage of your household income. So based on the table above, if you have a family of three and your household income is between $19,720 and $99,440, you will be eligible for a PTC. The actual PTC amount is based on the premium for the second-lowest-cost Silver plan available through the Marketplace. If you elect to buy more expensive coverage, such as a Gold or Platinum plan, you'd be responsible for the additional premium.

If your income falls within the FPL parameters, the premium you're required to pay for insurance purchased through a Marketplace is reflected as a percentage of your household income. So based on the table above, if you have a family of three and your household income is between $19,720 and $99,440, you will be eligible for a PTC. The actual PTC amount is based on the premium for the second-lowest-cost Silver plan available through the Marketplace. If you elect to buy more expensive coverage, such as a Gold or Platinum plan, you'd be responsible for the additional premium.

When you apply for insurance through a Marketplace, they will estimate the amount of your PTC based on information you provide. Before you actually apply for insurance, you can get an idea of whether you'll qualify for a PTC and, if you qualify, the approximate amount of the PTC by referring to the Kaiser Family Foundation calculator. This will show you the average cost of insurance for the second-lowest-cost Silver plan in a Marketplace and the amount of the credit. To apply the credit to other plans besides the Silver plan, you can get an estimate of the premium cost for insurance purchased through a Marketplace by going to the government website.

In addition to PTCs, the ACA also provides additional assistance to lower-income individuals through tax subsidies that reduce cost sharing by lowering point-of-service costs such as deductibles and co-payments. This is done by allowing families with incomes at or below 250% of FPL to be eligible for insurance with higher actuarial values, meaning the plan will pay for more of the covered benefits.

According to the government website, www.healthcare.gov, those eligible for cost-sharing subsidies must purchase a Silver plan through a Marketplace. However, the benefits covered by the plan will be comparable to either a Gold or Platinum plan, which pays for more of the covered benefits, reducing the out-of-pocket costs for the insured family. The percentage of benefits for which the plan will pay is as follows:

· For income between 100%-150% of FPL, the plan will pay 94% of covered benefits and the individual pays 6%

· For income between 150%-200% of FPL, the plan will pay 87% of covered benefits and the individual pays 13%

· For income between 200%-250% of FPL, the plan will pay 73% of covered benefits and the individual pays 27%

The ACA limits the total amount people must pay for essential benefits covered by nongrandfathered plans purchased through a Marketplace. For 2024, the limits are $9,450 for an individual plan and $18,900 for a family plan. These limits do not include premium costs or balance billing amounts for non-network providers and other out-of-network cost-sharing, or spending for non-essential health benefits.

The combination of PTCs and cost-sharing subsidies is intended to reduce the cost of insurance and increase the value of coverage available to individuals and families with moderate to low household incomes who don't have qualifying insurance coverage available through an employer.

What if your family size or income changes?

It's possible that after you purchase insurance through a Marketplace, your estimated PTC amount may change during the year due to changes in your family size or income. If your actual PTC is less than the estimated PTC, the difference will be subtracted from your tax refund or added to the tax due. And if your actual PTC is more than the estimated PTC, the difference will be added to your refund or subtracted from the tax due. If, during the policy year, you think your PTC will change, it's probably a good idea to notify the Marketplace, which can then make the adjustment instead of waiting until the end of the year.

*2023 FPL numbers are used to calculate PTCs for 2024.

Plans available through the Marketplace

There are five categories of health plans offered through the Marketplace, based on the percentage of the average overall costs for essential benefits the plan covers. You are responsible for the balance of the costs of benefits. The percentage of the cost for essential benefits paid by each plan is as follows:

· Bronze plan--60%

· Silver plan--70%

· Gold plan--80%

· Platinum plan--90%

Marketplaces also provide a Catastrophic plan, which meets all of the requirements of the other marketplace-based plans, but only provides coverage after the plan deductible is met, except for covering three primary care visits per year. These plans are only available to individuals under age 30 or those eligible for a "hardship exemption."

This content has been reviewed by FINRA.

Prepared by Broadridge Advisor Solutions. © 2024 Broadridge Financial Services, Inc.

Health-Care Reform: Credits and Subsidies

Tax credits available through Health Insurance Marketplace

Eligible individuals and families purchasing insurance through a Marketplace may be entitled to a premium tax credit (PTC) that can reduce the cost of insurance. If you qualify, you can elect to have the credit amount paid to your insurance company to decrease monthly premiums, or you can claim the PTC on your tax return.

Eligibility for tax credits

Eligibility for the PTC is based on the following requirements:

· You must be a U.S. citizen or have proof of legal residency and you must buy health insurance through a Marketplace

· Your household modified adjusted gross income is within a certain range based on the Federal Poverty Level (FPL)

· You are not eligible for minimum, qualifying insurance coverage through your employer or a government program such as Medicare or Medicaid

· If you are married, you and your spouse file a joint tax return

· You are not claimed as a dependent by another person

Tax credits and the federal poverty level

Whether you qualify for a PTC depends on your household income and family size. Income limits are based on a percentage of the FPL. Household income is your modified adjusted gross income (MAGI) plus the income of every other individual in your family who files an income tax return and for whom you claim a personal exemption deduction. MAGI is essentially your adjusted gross income plus any excluded foreign income, nontaxable Social Security benefits, and tax-exempt interest.

If your MAGI falls between 100% and 400% of the FPL, you may be entitled to a PTC. The following table illustrates the relationship between income as a percentage of FPL and household size. Incomes that qualify for tax credits are higher in Alaska and Hawaii.

If your income falls within the FPL parameters, the premium you're required to pay for insurance purchased through a Marketplace is reflected as a percentage of your household income. So based on the table above, if you have a family of three and your household income is between $19,720 and $99,440, you will be eligible for a PTC. The actual PTC amount is based on the premium for the second-lowest-cost Silver plan available through the Marketplace. If you elect to buy more expensive coverage, such as a Gold or Platinum plan, you'd be responsible for the additional premium.When you apply for insurance through a Marketplace, they will estimate the amount of your PTC based on information you provide. Before you actually apply for insurance, you can get an idea of whether you'll qualify for a PTC and, if you qualify, the approximate amount of the PTC by referring to the Kaiser Family Foundation calculator. This will show you the average cost of insurance for the second-lowest-cost Silver plan in a Marketplace and the amount of the credit. To apply the credit to other plans besides the Silver plan, you can get an estimate of the premium cost for insurance purchased through a Marketplace by going to the government website.

Cost-sharing subsidies

In addition to PTCs, the ACA also provides additional assistance to lower-income individuals through tax subsidies that reduce cost sharing by lowering point-of-service costs such as deductibles and co-payments. This is done by allowing families with incomes at or below 250% of FPL to be eligible for insurance with higher actuarial values, meaning the plan will pay for more of the covered benefits.

According to the government website, www.healthcare.gov, those eligible for cost-sharing subsidies must purchase a Silver plan through a Marketplace. However, the benefits covered by the plan will be comparable to either a Gold or Platinum plan, which pays for more of the covered benefits, reducing the out-of-pocket costs for the insured family. The percentage of benefits for which the plan will pay is as follows:

· For income between 100%-150% of FPL, the plan will pay 94% of covered benefits and the individual pays 6%

· For income between 150%-200% of FPL, the plan will pay 87% of covered benefits and the individual pays 13%

· For income between 200%-250% of FPL, the plan will pay 73% of covered benefits and the individual pays 27%

Out-of-pocket limit

The ACA limits the total amount people must pay for essential benefits covered by nongrandfathered plans purchased through a Marketplace. For 2024, the limits are $9,450 for an individual plan and $18,900 for a family plan. These limits do not include premium costs or balance billing amounts for non-network providers and other out-of-network cost-sharing, or spending for non-essential health benefits.

Conclusion

The combination of PTCs and cost-sharing subsidies is intended to reduce the cost of insurance and increase the value of coverage available to individuals and families with moderate to low household incomes who don't have qualifying insurance coverage available through an employer.

What if your family size or income changes?

It's possible that after you purchase insurance through a Marketplace, your estimated PTC amount may change during the year due to changes in your family size or income. If your actual PTC is less than the estimated PTC, the difference will be subtracted from your tax refund or added to the tax due. And if your actual PTC is more than the estimated PTC, the difference will be added to your refund or subtracted from the tax due. If, during the policy year, you think your PTC will change, it's probably a good idea to notify the Marketplace, which can then make the adjustment instead of waiting until the end of the year.

*2023 FPL numbers are used to calculate PTCs for 2024.

Plans available through the Marketplace

There are five categories of health plans offered through the Marketplace, based on the percentage of the average overall costs for essential benefits the plan covers. You are responsible for the balance of the costs of benefits. The percentage of the cost for essential benefits paid by each plan is as follows:

· Bronze plan--60%

· Silver plan--70%

· Gold plan--80%

· Platinum plan--90%

Marketplaces also provide a Catastrophic plan, which meets all of the requirements of the other marketplace-based plans, but only provides coverage after the plan deductible is met, except for covering three primary care visits per year. These plans are only available to individuals under age 30 or those eligible for a "hardship exemption."

This content has been reviewed by FINRA.

Prepared by Broadridge Advisor Solutions. © 2024 Broadridge Financial Services, Inc.