Financial Planning

back

As expected, Medicare costs will increase in 2025 “due to projected price changes” and an increase in the number of people using health care services.

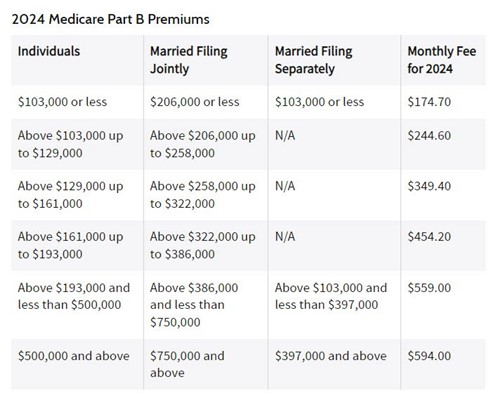

Seniors will pay 2.7% more for hospital stays with Part A coverage. Monthly premiums for medical coverage (Part B) will also rise by 5.9%, from $174.70 to $185 in 2025, and seniors who use these services will pay 7.1% higher deductibles, from $240 to $257 in 2025.1

Some Medicare Supplement plans, which you can buy to help cover your out-of-pocket Medicare costs, may cover deductibles, but none cover the Part B premium.

You can switch from Original Medicare (Parts A and B) to Medicare Advantage (Part C) during the Medicare open enrollment period, which is going on now and lasts each year from Oct. 15 to Dec. 7.

Medicare Part A covers inpatient hospital stays, as well as nursing facilities, home health care, and hospice care. Most people don’t pay any premiums for Part A because they’ve been paying Medicare taxes for at least 10 years during their working years, which is usually enough to waive the Part A premium.

If you need to pay, the Part A premium in 2025 can be up to $518 a month, a $13 increase from 2024. The exact amount depends on how long you or your spouse paid Medicare taxes. People who worked between 30 quarters (7.5 years) and 10 years pay a lower premium of $285.1

Everyone, however, will have a deductible. Here’s how the deductibles are changing in 2025:

The Medicare Part A deductible works similarly to private health insurance: You’re responsible for paying the deductible out of pocket before Medicare coverage kicks in. Unlike most health insurance deductibles, the Part A deductible applies to each individual facility stay, known as a “benefit period.”

Once you’ve paid your deductible for that particular stay, you’ll begin paying “coinsurance” instead. It’s a fixed price depending on how long that stay has lasted and the type of facility you’re in.

If you don’t have many assets and your income is very low, you may qualify for some or all of your Medicare costs to be paid through Medicaid, although the rules and benefits vary by state.

You may have to pay the deductible more than once if you have multiple hospital stays per year. For example, if you’re hospitalized in January 2025 for two weeks with a bad case of the flu, you’d have to pay your deductible ($1,676), but you wouldn’t owe anything else since coinsurance isn’t required for hospital stays under 60 days. But if you suffer an accident later in May 2025 and require a three-month hospital stay, you’d pay your deductible again ($1,676), plus $419 daily starting on day 61.

Part B covers regular medical care, such as doctor’s visits, vaccinations, medical equipment, outpatient procedures, and more.

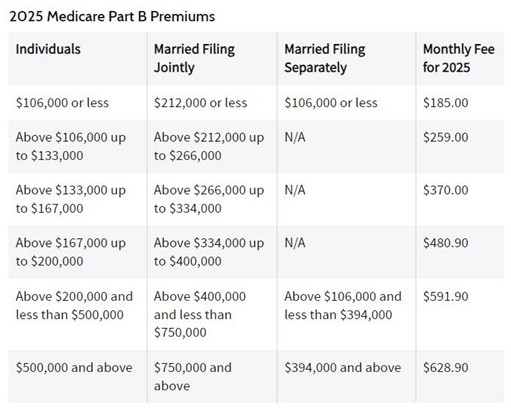

Your Part B premium depends mainly on your income, as measured by your modified adjusted gross income (MAGI) using your most recent tax return. The higher your MAGI, the higher your Part B premium.

Most people pay a base amount, but if you have a higher income in retirement from investment income, a pension, or other sources, you might pay more. Your Medicare Part B premiums start to increase once your modified adjusted gross income (MAGI) reaches $106,000 (for individuals and married couples filing separately) or $212,000 (for married couples who file joint tax returns) based on your most recent tax return.1

If you’re signed up for Original Medicare, your Part B premiums will automatically be taken out of your Social Security checks. If you’re signed up for another plan, such as Part C (i.e., Medicare Advantage) or Part D, you can opt to take these out of your Social Security checks or pay them directly.

Here’s how much you’ll pay for premiums for Medicare Part B coverage in 2025:

Note that if you’re married but file separate tax returns and have lived away from your spouse for the last year, you may file as an individual taxpayer and pay premiums as such.

In comparison, here are the Medicare Part B premiums from 2024:2

Your deductible and coinsurance costs for Part B coverage work differently than for Part A. Your deductible applies for medical care during the whole year rather than for each separate visit. You’ll also pay a coinsurance of 20% for most services.3

Here’s how the deductibles and coinsurance amounts are changing in 2025:

In addition to changing premiums and deductibles for Original Medicare coverage, there are lots of new Medicare changes being introduced in 2025. Many of these apply to Medicare Advantage plans, but some apply to all Medicare options:

Seniors receiving Social Security will see their benefit amount increase by 2.5% in 2025 due to the yearly cost-of-living adjustment. However, since Medicare premiums are often taken directly from your Social Security payment, you may see smaller monthly checks in 2025 due to the 5.9% increase in Medicare Part B premiums. These changes are in line with historical trends from 2000 to 2018, where average Social Security payments rose by 2.2% per year, while Medicare costs increased at a faster rate of 6.1% annually.

It’s also important to remember that if you need to use your coverage, it may be more expensive due to the rise in deductibles. You may need to adjust your budget for higher out-of-pocket healthcare spending in 2025.

Experts also recommend checking out your options for Medicare Advantage plans, which may come with different costs that better align with your budget and needs. You can change your Medicare plan during the open enrollment period from Oct. 15 to Dec. 7. If you elect to change plans, your coverage (and costs) will take effect starting on Jan. 1 in the new year.

If you already have a Medicare Advantage plan, it’s important to review any changes in your plan’s coverages and costs, especially when it comes to your insurer’s formulary of prescription drugs. Some of the changes that Medicare requires in 2025, such as caps on drug spending, may cause private insurers to reduce coverage and increase costs. The Centers for Medicare & Medicaid Services doesn’t expect this to happen on a widespread scale, but it’s still important to read your plan’s annual notice of changes letter to get all the details.

Article Sources

Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in our editorial policy.

1. CMS. “2025 Medicare Parts A & B Premiums and Deductibles.”

2. CMS. “2024 Medicare Parts A & B Premiums and Deductibles.”

3. Medicare. “Costs.”

Medicare Costs Are Going Up in 2025—Here's the Impact on Your Wallet

Key Takeaways

- Medicare Part A (hospital insurance) deductibles will rise by 2.7% in 2025.

- Part B (medical coverage) premiums will rise by 5.9%, while deductibles will increase by 7.1% in 2025.

- Everyone has to pay Part B premiums, even if you have a Medicare Advantage plan.

- You can make changes to your 2025 Medicare plan during open enrollment, which lasts from Oct. 15–Dec. 7, 2024.

As expected, Medicare costs will increase in 2025 “due to projected price changes” and an increase in the number of people using health care services.

Seniors will pay 2.7% more for hospital stays with Part A coverage. Monthly premiums for medical coverage (Part B) will also rise by 5.9%, from $174.70 to $185 in 2025, and seniors who use these services will pay 7.1% higher deductibles, from $240 to $257 in 2025.1

Some Medicare Supplement plans, which you can buy to help cover your out-of-pocket Medicare costs, may cover deductibles, but none cover the Part B premium.

You can switch from Original Medicare (Parts A and B) to Medicare Advantage (Part C) during the Medicare open enrollment period, which is going on now and lasts each year from Oct. 15 to Dec. 7.

Part A Costs

Medicare Part A covers inpatient hospital stays, as well as nursing facilities, home health care, and hospice care. Most people don’t pay any premiums for Part A because they’ve been paying Medicare taxes for at least 10 years during their working years, which is usually enough to waive the Part A premium.

If you need to pay, the Part A premium in 2025 can be up to $518 a month, a $13 increase from 2024. The exact amount depends on how long you or your spouse paid Medicare taxes. People who worked between 30 quarters (7.5 years) and 10 years pay a lower premium of $285.1

Everyone, however, will have a deductible. Here’s how the deductibles are changing in 2025:

The Medicare Part A deductible works similarly to private health insurance: You’re responsible for paying the deductible out of pocket before Medicare coverage kicks in. Unlike most health insurance deductibles, the Part A deductible applies to each individual facility stay, known as a “benefit period.”

Once you’ve paid your deductible for that particular stay, you’ll begin paying “coinsurance” instead. It’s a fixed price depending on how long that stay has lasted and the type of facility you’re in.

If you don’t have many assets and your income is very low, you may qualify for some or all of your Medicare costs to be paid through Medicaid, although the rules and benefits vary by state.

You may have to pay the deductible more than once if you have multiple hospital stays per year. For example, if you’re hospitalized in January 2025 for two weeks with a bad case of the flu, you’d have to pay your deductible ($1,676), but you wouldn’t owe anything else since coinsurance isn’t required for hospital stays under 60 days. But if you suffer an accident later in May 2025 and require a three-month hospital stay, you’d pay your deductible again ($1,676), plus $419 daily starting on day 61.

Part B Costs

Part B covers regular medical care, such as doctor’s visits, vaccinations, medical equipment, outpatient procedures, and more.

Your Part B premium depends mainly on your income, as measured by your modified adjusted gross income (MAGI) using your most recent tax return. The higher your MAGI, the higher your Part B premium.

Most people pay a base amount, but if you have a higher income in retirement from investment income, a pension, or other sources, you might pay more. Your Medicare Part B premiums start to increase once your modified adjusted gross income (MAGI) reaches $106,000 (for individuals and married couples filing separately) or $212,000 (for married couples who file joint tax returns) based on your most recent tax return.1

If you’re signed up for Original Medicare, your Part B premiums will automatically be taken out of your Social Security checks. If you’re signed up for another plan, such as Part C (i.e., Medicare Advantage) or Part D, you can opt to take these out of your Social Security checks or pay them directly.

Here’s how much you’ll pay for premiums for Medicare Part B coverage in 2025:

Note that if you’re married but file separate tax returns and have lived away from your spouse for the last year, you may file as an individual taxpayer and pay premiums as such.

In comparison, here are the Medicare Part B premiums from 2024:2

Part B Deductible and Coinsurance

Your deductible and coinsurance costs for Part B coverage work differently than for Part A. Your deductible applies for medical care during the whole year rather than for each separate visit. You’ll also pay a coinsurance of 20% for most services.3

Here’s how the deductibles and coinsurance amounts are changing in 2025:

How Medicare Is Changing in 2025

In addition to changing premiums and deductibles for Original Medicare coverage, there are lots of new Medicare changes being introduced in 2025. Many of these apply to Medicare Advantage plans, but some apply to all Medicare options:

- Prescription drug savings: Starting in 2025, your out-of-pocket costs for prescription drug coverage under Part D are capped at $2,000 per year, and you can opt to pay these charges with a monthly payment plan.

- Mid-year Medicare Advantage statements: If you’re signed up for a Medicare Advantage plan, you’ll get a statement halfway through the year showing which benefits you still have available. These benefits are a big lure of these plans, yet many people don’t fully use them.

- Increased benefits for dementia caregivers: Families caring for dementia patients can receive up to $2,500 each year for respite services, as well as access to caregiver training and a care navigator to help find other support options.

- More mental health care options: Medicare Advantage enrollees will now be able to visit licensed marriage and family therapists, mental health counselors, and addiction treatment providers, all of whom weren’t previously able to bill Medicare for services.

How the Changes Affect You

Seniors receiving Social Security will see their benefit amount increase by 2.5% in 2025 due to the yearly cost-of-living adjustment. However, since Medicare premiums are often taken directly from your Social Security payment, you may see smaller monthly checks in 2025 due to the 5.9% increase in Medicare Part B premiums. These changes are in line with historical trends from 2000 to 2018, where average Social Security payments rose by 2.2% per year, while Medicare costs increased at a faster rate of 6.1% annually.

It’s also important to remember that if you need to use your coverage, it may be more expensive due to the rise in deductibles. You may need to adjust your budget for higher out-of-pocket healthcare spending in 2025.

Experts also recommend checking out your options for Medicare Advantage plans, which may come with different costs that better align with your budget and needs. You can change your Medicare plan during the open enrollment period from Oct. 15 to Dec. 7. If you elect to change plans, your coverage (and costs) will take effect starting on Jan. 1 in the new year.

If you already have a Medicare Advantage plan, it’s important to review any changes in your plan’s coverages and costs, especially when it comes to your insurer’s formulary of prescription drugs. Some of the changes that Medicare requires in 2025, such as caps on drug spending, may cause private insurers to reduce coverage and increase costs. The Centers for Medicare & Medicaid Services doesn’t expect this to happen on a widespread scale, but it’s still important to read your plan’s annual notice of changes letter to get all the details.

Article Sources

Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in our editorial policy.

1. CMS. “2025 Medicare Parts A & B Premiums and Deductibles.”

2. CMS. “2024 Medicare Parts A & B Premiums and Deductibles.”

3. Medicare. “Costs.”